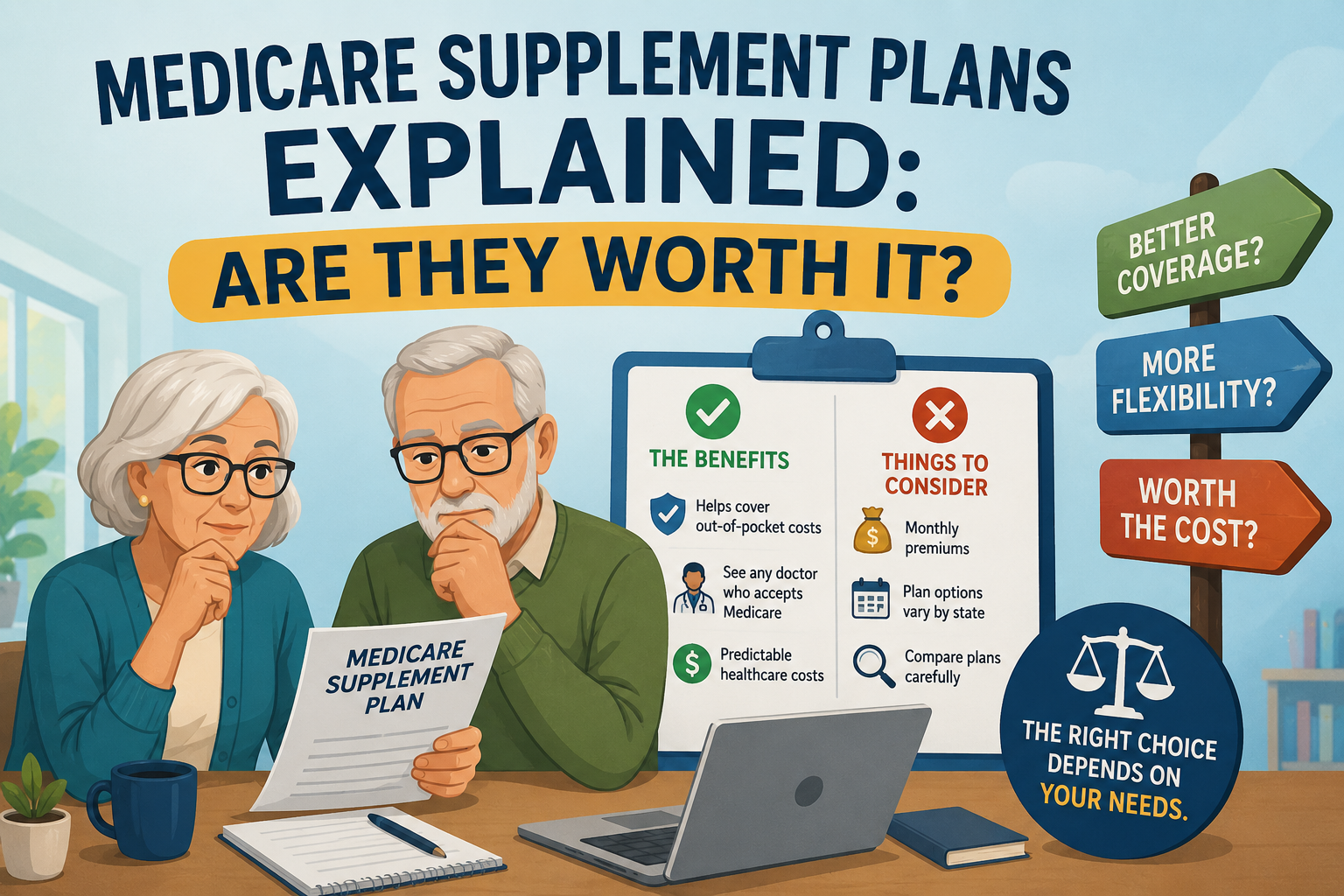

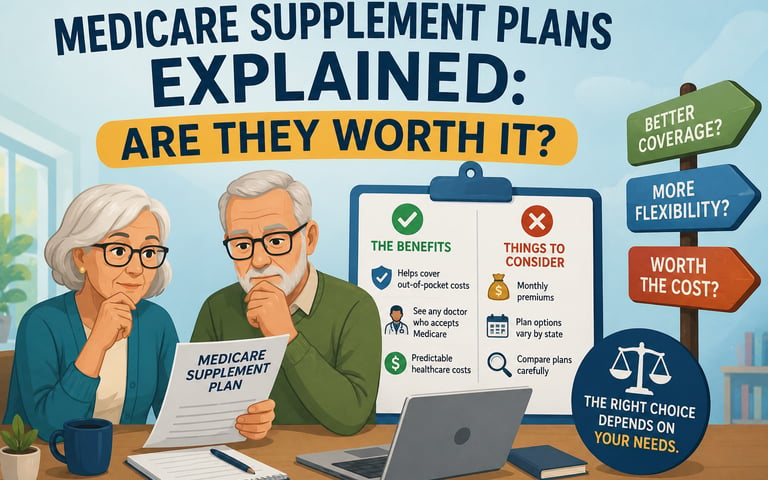

Medicare Supplement Plans Explained: Are They Worth It?

Medicare Supplement plans help cover many of the costs Original Medicare does not pay, like deductibles and copays. They can offer more predictable healthcare expenses and flexibility with doctors nationwide. This article explains how Supplements work, their pros and cons, and how to decide if one may fit your needs.

MEDICARE SUPPLEMENT PLANS

When people first start learning about Medicare, one of the biggest questions they ask is:

“Do I need a Medicare Supplement plan?”

The answer depends on your health needs, budget, and how much predictability you want when it comes to medical bills. There is no one-size-fits-all answer, but understanding how Supplement plans work can help you decide whether they fit your situation.

What Is a Medicare Supplement Plan?

A Medicare Supplement plan — also called a Medigap plan — works alongside Original Medicare (Parts A & B).

Original Medicare helps cover many healthcare costs, but it does not pay for everything. You are still responsible for deductibles, copays, coinsurance, and other out-of-pocket expenses.

A Supplement plan helps pay many of those leftover costs.

These plans are designed to give people more predictable healthcare expenses and peace of mind when unexpected medical needs come up.

How Supplements Work

With a Supplement plan:

You keep Original Medicare

You can usually see any doctor nationwide who accepts Medicare

Referrals are typically not required

Out-of-pocket costs are often much lower and more predictable

Many people like Supplements because they provide flexibility and simplicity, especially if they travel often or want broad doctor access.

What Supplement Plans Do NOT Include

Supplement plans generally do not include:

Prescription drug coverage

Dental

Vision

Hearing benefits

That means many people pair a Supplement with a separate Part D prescription drug plan.

Are Supplements Better Than Medicare Advantage?

This is one of the most common Medicare questions — and honestly, there is no single “best” option.

Medicare Advantage plans and Supplement plans both have pros and cons.

Supplement plans often have:

Higher monthly premiums

Lower out-of-pocket costs when you use care

More provider flexibility

Medicare Advantage plans often have:

Lower monthly premiums

Network restrictions

Copays as you use services

Extra benefits like dental or vision

The right fit depends on your doctors, prescriptions, budget, travel habits, and comfort level with risk.

When a Supplement Plan May Make Sense

A Supplement plan may be worth considering if:

You want predictable medical costs

You travel frequently

You want freedom to see doctors nationwide

You dislike referrals or networks

You expect ongoing medical care

Peace of mind matters more than having the lowest premium

The best Medicare decision is not about choosing the most advertised plan or the cheapest premium.

It is about choosing coverage that fits your life.

That is why I take the time to look at the full picture — your doctors, medications, budget, and what matters most to you long term. Medicare has real moving parts, and having someone in your corner can make the process a lot less overwhelming.

If you have questions about Supplements, Medicare Advantage, or just want help understanding your options, I’m always happy to help.

Shawn Ray Insurance

We do not offer every plan available in your area. Any information we provide is limited to those plans we do offer in your area. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.

Medicare Guidance with Personal, year-round support.

Serving clients in most states across the nation.

Helpful Links

Ways to Reach Me

Text or Call:

Shawn.Ray@medicareadvocates.com